Whether you’re a developer looking for a fast and flexible way to light a new housing project or a municipality looking to reduce infrastructure costs and meet sustainability goals, there has never been a better time to invest in solar lighting.

That might sound like a ‘line’ coming as it is from a company with a vested interest in selling solar lighting products but hear us out. There’s a newly expanded federal tax incentive that can offset 30% (or more) of the cost of a solar lighting installation. Businesses, state and local governments, and tribal councils are all eligible, and virtually all expenses—equipment, labor, tax—can be claimed. New “direct pay” and “transferability” provisions make it easier than ever to access funding, without needing to involve third-party investors and ‘equity owners’.

So, what is this potent solar incentive? It’s called the Investment Tax Credit (ITC) and it’s been called everything from an “underrated tool” to “one of the most important federal policy mechanisms to incentivize clean energy in the United States.” In this article, we’ll explain how it works, what and who is eligible, and some strategies for maximizing your pay-out.

The ITC, technically called the Energy Investment Tax Credit, is a tax credit that reduces the federal income tax liability for a percentage of the cost of a solar system in the year it’s installed. Though not new—it was originally enacted under the Bush Administration in 2005 to encourage homeowners to adopt energy technologies—it was recently extended and expanded under the Inflation Reduction Act (IRA) in some significant ways.

Most importantly, it opened the ITC to non-taxpaying entities (municipalities, non-profits, tribal councils, etc.) which have not historically benefited from tax credits. It also added a new “direct pay” provision that allows these organizations to receive a cash refund equal to the credit’s value (rather than subtract it from a tax balance they don’t have). And, for developers not eligible for direct pay, the IRA made the ITC “transferable,” meaning they can sell their tax credits to an unrelated party for cash. More on that below.

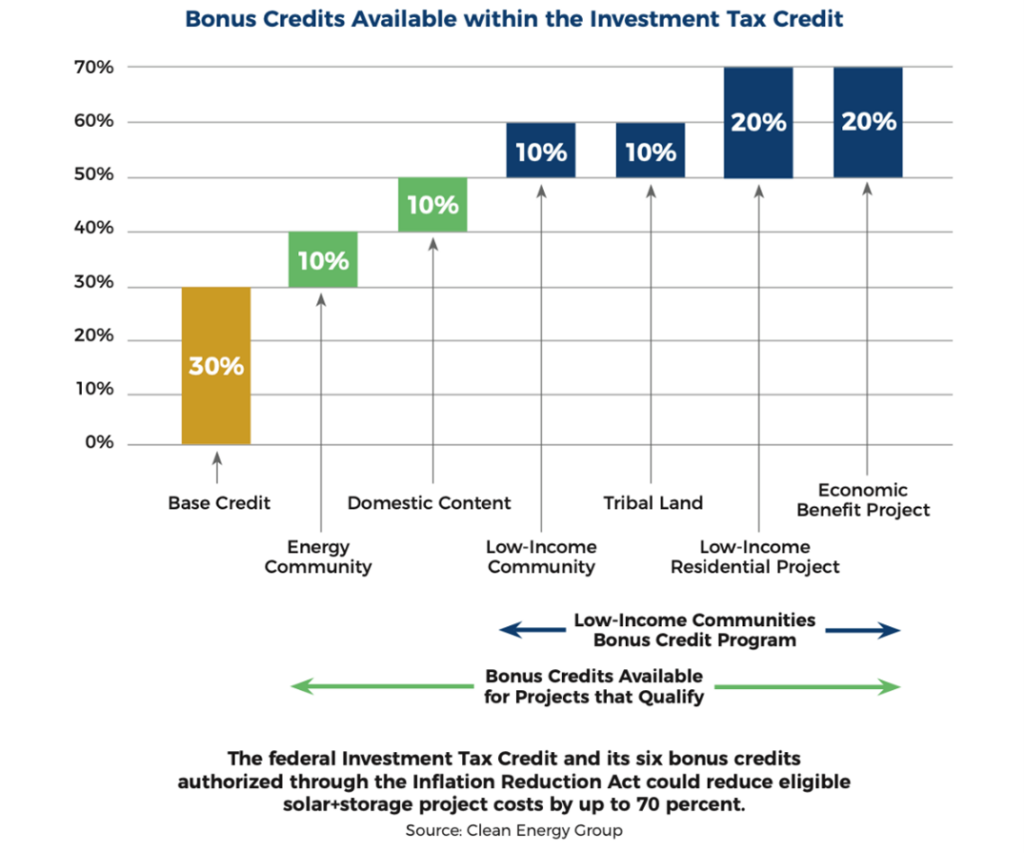

We dropped a hint in the intro, but the answer is the most annoying of responses: It depends! In theory, up to 70% of qualifying product costs can be covered by the ITC and its bonus credit amounts. However, it can be as low as 30% (still pretty good!) if none of the bonus criteria are met. Here’s what you need to know to maximize your credit amount:

Source: Clean Energy States Alliance

Note that these bonuses stack, so a project that meets all the bonus requirements could cover most of its costs using the ITC. To calculate your credit amount, you multiply the applicable tax credit percentage (say, 50% because you’ve purchased one of Sol’s American-made systems and your project is on Tribal land) by the amount spent on the asset. A $90k solar installation would qualify for a $45k credit/refund!

Also, note that the credit won’t be around forever. The IRA outlines a phased reduction in the ITC percentage over time, with systems placed in service in the next ten years eligible for the full 30% base credit before reducing to 22.5% in 2034, 15% in 2035, and ultimately zeroing out in 2036.

While our focus is obviously on solar, a wide range of clean energy technologies are eligible for the ITC, including geothermal, fuel cell, microturbine, small wind, offshore wind, tidal, biogas… you get the idea. If it’s renewable, located in the U.S., installed between 2023 and 2034, and uses new (and limited previously used) equipment, chances are it’s eligible for the ITC.

The DOE has a comprehensive list if you’re wondering exactly which expenses can be claimed. For solar lighting projects, you can claim the entire asset value (including solar panels, batteries, mounting equipment, and wiring), installation costs, and sales tax.

Back to those IRA updates we introduced earlier. First, the IRA authorized tax-exempt entities to opt for cash payments instead of tax credits using a provision called “direct pay.” Although these entities were technically eligible for the ITC before the IRA, they were forced to partner with for-profit investors because they had no taxable income. Now, they can access the credit (or cash) directly, which the National League of Cities (NLC) says will “level the playing field between local governments and the private sector.”

Graphic adapted from the Environmental and Energy Study Institute

Second, the IRA made the ITC “transferable,” allowing most taxpayers (i.e. those excluded from direct pay) to sell their credits to an unrelated party. If you’re wondering why (we were!), it’s because, pre-IRA, many developers didn’t have enough tax liability to use the credit fully. They, too, often ended up partnering with a third party (in this case, a tax equity investor) with sufficient liability to take advantage of the credit. There are a bunch of reasons this isn’t ideal, but the bottom line is it just got a lot simpler for developers with limited tax capacity to access the ITC, and we say that’s a win!

Yes! We’ve written 1,200 words on the ITC because we think it’s the most compelling incentive available to prospective solar lighting customers, but it’s far from the only one. The Bipartisan Infrastructure Law (BIL) created and expanded a slew of federal funding programs, many of which can be applied to renewable energy infrastructure (check out the Energy Efficiency and Conservation Block Grant Program and Safe Streets and Roads for All).

Another great tool is the Database of State Incentives for Renewables and Efficiency (DSIRE), which aggregates information on incentives and policies that support renewables at the federal, state, local, and utility levels. According to the DOE, “Most solar system rebates provided by a utility or state government are considered taxable income and do not change the tax basis when calculating the ITC.” So, if the qualifying cost of an asset is $90k and the applicable tax credit percentage is 50%, the credit is $45k whether you receive an additional $20k grant from the state or not.

Whether you’re a federal employee, city engineer, or private developer, there truly hasn’t ever been a better time to invest in solar lighting. The ITC is essentially free money for your next project—but as we’ve mentioned, it won’t be available forever. Many of our customers are already seeing the benefits of leveraging the credit to build solar projects that save energy, reduce costs, and increase safety.

Do you want to be next? Our team of solar experts would love to help.

Have you already installed a solar lighting system this year? You can claim it on this years’ taxes!